Pensions of millions of Ukrainians are at risk: how to save for a comfortable life.

According to The Sun: Experienced economist Joan Gascoigne managed to save an impressive amount – £220,000 thanks to the golden rule of saving 15%.

To save without undue pressure, she used a helpful app. Here’s how she did it and tips from financial experts to help boost your savings.

Joan Gascoigne adheres to a strict budget and does not buy new clothes in stores to save as much as possibleJoan, 46, a business consultant from Sheffield, decided to set aside money to avoid worrying about finances during retirement.

She started saving for retirement at 21, now saving 15% of her income, which is about £500 a month.

Financial experts recommend following this golden rule to ensure a comfortable life in retirement. Her employer also contributes to her pension fund.

Joan is already more than halfway to achieving the necessary amount to maintain her standard of living in retirement, as she does not want to worry about money in old age.

“My lifestyle is based on planning, not spontaneity. I spend only on what is truly important, and save the rest for the future,”– she said.

To save £500 a month, Joan closely monitors her expenses.

She buys clothes exclusively on Vinted, instead of buying new ones.

Joan also uses the Plum saving app, which helped her save nearly £10,000 over three years – most of which she directed to her pension.

Plum connects to your bank account and determines how much you can afford to save, automatically setting aside that amount. This allows you to save without even realizing it.

Money is stored in an accessible savings account in the app with an interest rate of 3.53%. However, Joan has chosen to direct most of her funds towards retirement.

Another advantage of saving for retirement is that it is one of the most efficient ways to save due to tax benefits, which means more money in your pocket.

The benefit for basic rate taxpayers, like Joan, is 25% – which means that for every £80 you save, the government adds another £20.

Thus, her fund has also benefited from significant compound interest, meaning you earn more as your capital grows.

Joan also uses the online store Vinted to control her expensesAlamy“To save consistently took a lot of effort and discipline, but I hope it will allow me to be comfortable and not worry about money in the future,”– she noted.

Joan is not the only one worrying about whether she will have enough money to live on after retirement.

About 15 million people are not saving enough, according to government estimates, and the situation is only getting worse.

Retirees who are set to retire in 2050 will be around £800 poorer per year compared to those who are finishing work today.

Savers feel the pressure: half of people are worried that their retirement savings won't last a lifetime, according to data from investment company Investec Wealth & Investment.

But don’t worry – leading financial experts have several key tips to improve your savings. They suggest how to get an additional £342 a year in state pension payments and emphasize the importance of the 15% rule.

Step one – determine how much you need to save

Determining how much you need for retirement can be tricky, as everyone’s circumstances are different.

But experts offer general advice that can help you figure out how much you need for a comfortable life.

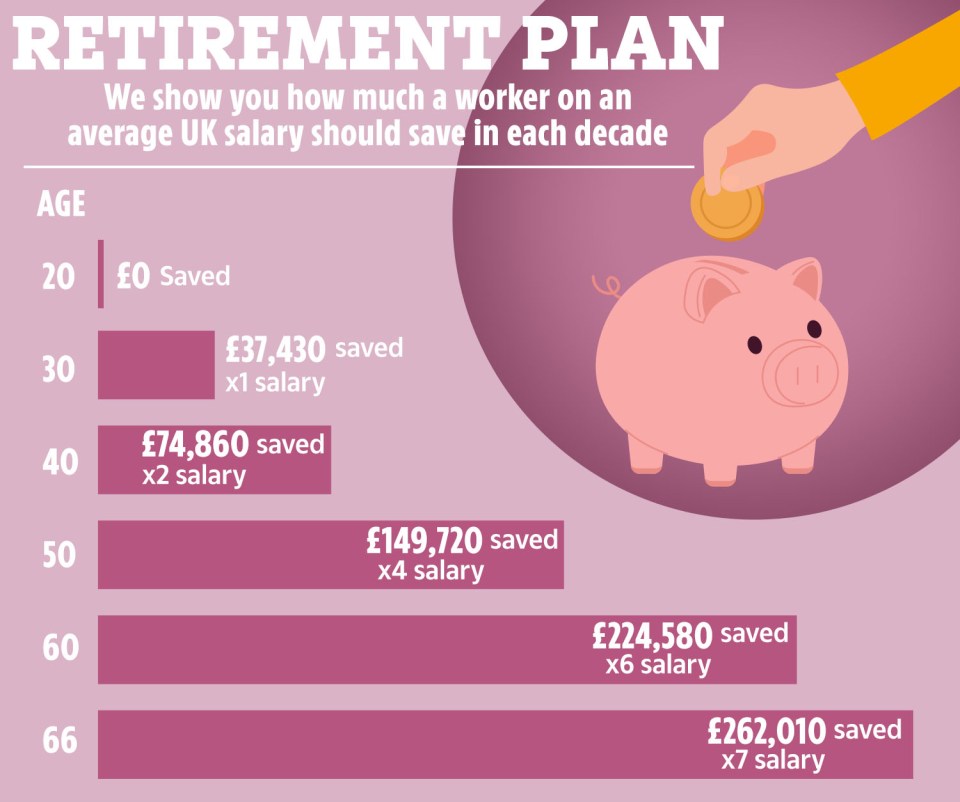

The Pension and Life Association states that a single person needs £13,400 (£21,600 for a couple) for a “minimum” pension, covering basic needs, utility bills, and allowing for some money for a small vacation or a budget meal once a month.

- £28,000 for minimum pension

- £415,000 for moderate pension

- £682,000 for comfortable pension

Step two – check your pension fund

Now that you know how much to save, the next step is to check how much you already have in your pension fund.

You may have lost track of your fund.

There is about £31.1 billion lying in inactive or “lost” pension funds that are either forgotten or the saver cannot find them.

Review your employment history and check if you know where your pension fund is for each company.

Step three – review your pension

There are many ways you can increase your income from a private pension.

One of the simplest ways is to make more contributions to your pension fund and start saving as early as possible – you will have more time for your capital to grow.

The minimum amount you should contribute to your fund is 5% of your annual salary, while your employer should contribute 3%.

Additionally, the government tops up your pension contributions by 25%, known as the ‘pension tax relief’, so you essentially get two free cash contributions.

Step four – increase your state pension

Don’t forget about the state pension – it forms the foundation of many retirement plans and amounts to a maximum of £11,973 per year.

To increase your total retirement income, it is important to ensure you qualify for the maximum state pension.

You need 35 years of National Insurance contributions to receive the maximum amount, and at least 10 years to receive anything at all.

Check your records if you are unsure that you have enough qualifying years.

If you have not accumulated enough years, you can pay to top up your records, increasing your pension income.

Additional information is available on government websites.

This news highlights the importance of financial planning for retirement and simple yet effective ways to save. In a world where many people lack sufficient savings for old age, Joan Gascoigne's experience can serve as an example for others seeking to secure their financial well-being in the future. Using tools such as savings apps can yield impressive results, even without putting in a lot of effort.

This news highlights the importance of financial planning for retirement and simple yet effective ways to save. In a world where many people lack sufficient savings for old age, Joan Gascoigne's experience can serve as an example for others seeking to secure their financial well-being in the future. Using tools such as savings apps can yield impressive results, even without putting in a lot of effort. Read also

- Global Fuel Markets Shaken as Ukrainian Drones Undermine Russian Control

- Russian Business Owners Are Moving Billions Abroad Amid Fears of Asset Seizure and Forced War Funding

- Former Minister Sobolev Takes on New Role in the President’s Office: What He Will Be Working On

- India Becomes Fuel Supplier to Russia as Diesel Shortage Bites

- Currency Panic Grips Ukraine: Expert Reveals Why People Are Losing Faith in the Hryvnia

- Major Salary Hikes Planned for Ukrainian Rescuers: Here’s What They Could Earn